All Categories

Featured

There is no one-size-fits-all when it comes to life insurance. Getting your life insurance policy plan appropriate takes into consideration a number of variables. [video description: Pleasant music plays as Mark Zagurski speaks to the camera.] In your active life, financial independence can feel like an impossible goal. And retired life might not be top of mind, due to the fact that it seems thus far away.

Pension plan, social security, and whatever they 'd managed to save. But it's not that simple today. Less employers are supplying conventional pension and lots of firms have actually reduced or stopped their retirement strategies and your ability to rely entirely on social security remains in question. Also if benefits have not been decreased by the time you retire, social safety alone was never ever meant to be enough to spend for the way of living you desire and are worthy of.

/ wp-end-tag > As part of an audio financial strategy, an indexed global life insurance coverage plan can aid

you take on whatever the future brings. Prior to dedicating to indexed universal life insurance coverage, below are some pros and disadvantages to take into consideration. If you pick a great indexed global life insurance strategy, you might see your cash money value expand in worth.

Universal Way Insurance

If you can access it early on, it might be advantageous to factor it right into your. Given that indexed global life insurance policy needs a certain degree of risk, insurance policy firms have a tendency to maintain 6. This sort of plan likewise offers (adjustable premium life insurance). It is still ensured, and you can readjust the face amount and motorcyclists over time7.

Generally, the insurance coverage firm has a vested rate of interest in doing much better than the index11. These are all elements to be considered when picking the best type of life insurance coverage for you.

Universal Whole

However, considering that this kind of plan is a lot more complex and has an investment element, it can typically feature higher premiums than other policies like whole life or term life insurance policy. If you do not believe indexed global life insurance coverage is ideal for you, below are some options to consider: Term life insurance policy is a temporary plan that generally provides insurance coverage for 10 to three decades.

When determining whether indexed universal life insurance policy is best for you, it's crucial to think about all your options. Entire life insurance policy may be a better option if you are seeking more security and uniformity. On the other hand, term life insurance policy might be a much better fit if you just need protection for a particular period of time. Indexed universal life insurance policy is a kind of policy that uses a lot more control and flexibility, along with higher cash money value development possibility. While we do not offer indexed global life insurance policy, we can give you with even more info concerning whole and term life insurance policy policies. We advise discovering all your alternatives and chatting with an Aflac representative to discover the ideal suitable for you and your family members.

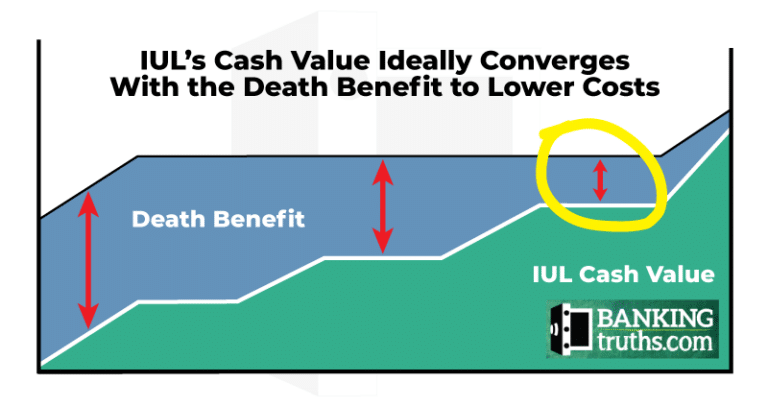

The rest is contributed to the money value of the plan after fees are subtracted. The cash value is attributed on a month-to-month or annual basis with rate of interest based upon increases in an equity index. While IUL insurance policy might prove useful to some, it is very important to comprehend how it functions before purchasing a plan.

{kind=link}

Latest Posts

Index Linked Insurance Products

Iul Insurance Meaning

Aseguranza Universal